{kind=link}

Proof from Canadathe United States and Europe exhibits that weather-related disasters aren’t skilled equally. The folks hardest hit are sometimes these with the fewest assets to manage.

Decrease-income and marginalized populations face higher publicity, have fewer assets to organize or get well and incur a better proportion of losses not lined by insurance coverage.

Even when they’re insured, many individuals have problem masking the deductible as a result of they lack emergency financial savings. This implies harm just isn’t repaired, folks dwell in unsafe or unhealthy situations and the monetary and private danger of future occasions is elevated.

Insurance coverage helps households get well and might forestall them from falling — or falling deeper — into poverty after a catastrophe. However throughout Canada, insurance coverage is changing into costlier and, in some locations, tougher to get. Between 2019 and 2023, common residence insurance coverage premiums rose by 21% general. For lower-income Canadians, that improve was 40%.

Widening Safety Hole

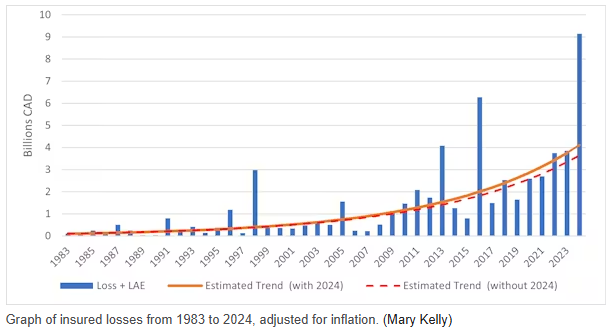

Canada’s rising insurance coverage safety hole is a severe concern, and it’s widening at a time when weather-related disasters are changing into extra frequent and extra extreme.

When households are uninsured, losses can pressure family budgets and go away folks unable to fulfill their primary wants. As excessive climate escalates, so does the chance that extra households will discover themselves unable to get well.

Affordability is the first driver of the safety hole, however it’s not the one one. Many Canadians don’t perceive the advantages of insurance coverage, or underestimate the likelihood and price of struggling a loss.

Accessibility to insurance coverage can also be a problem, particularly in distant areas the place it’s often bought in particular person. Whereas the expansion of digital buying channels helps, it’s not an answer for these with out dependable web or ample digital abilities.

Lastly, the market itself doesn’t all the time meet the wants of low-income or in any other case marginalized teams. There’s a lack of insurance coverage merchandise designed for these teams, leaving many with out the safety they want.

Strengthening Neighborhood Resilience

Higher insurance coverage choices, stronger investments in mitigation and higher assist for customers may help scale back inequities and strengthen resilience.

Neighborhood-level mitigation is an efficient place to begin. Land-use planning that steers growth away from high-risk areas can forestall future losses. Packages like FireSmartwhich reduces wildfire losses, and infrastructure designed for a altering local weather additionally assist restrict harm as extreme climate turns into extra frequent.

Nationwide assessments present that making housing extra resilient reduces publicity for lower-income and marginalized households which can be extra prone to dwell in older or poorly maintained houses, placing them at higher danger.

Whereas main retrofits might be expensive, even small upgrades equivalent to enhancing drainage, putting in backwater valves or fire-resistant supplies may help forestall harm. Many municipalities present focused subsidies and incentive applications that assist these upgrades, significantly for households dealing with higher monetary constraints.

Making hazard info simpler to seek out and perceive also can assist guarantee nobody is left behind when disasters strike. Many Canadians lack clear details about the hazards they face and easy methods to put together for them. Some residents, together with newcomers and seniors, could face boundaries in accessing or appearing upon out there info.

Lastly, neighborhood helps can additional strengthen resilience. Individuals with robust social ties and entry to neighborhood organizations get well extra shortly after disasters. Packages that construct native networks and assist neighbourhood teams may help accomplish this at a comparatively low value.

Closing the Safety Hole

A vital step in lowering the unequal impacts of weather-related hazards is closing Canada’s insurance coverage safety hole. Microinsurance is one promising resolutionand these simplified, low-cost insurance policies can present primary safety at a fraction of the fee for households that can’t afford conventional protection.

Embedded tenant insurance coverage — routinely included when renters signal a lease — is one other strategy that ensures primary protection.

Digital instrumentsequivalent to mobile-friendly sign-up platforms and plain-language coverage explanations, can scale back boundaries for many who wrestle with know-how.

Public assist for income-tested premium subsidies or credit can convey important protection inside attain for low-income households, whereas community-based disaster insurance coverage — the place native governments or neighborhood teams prepare protection on behalf of residents — presents another choice.

Whereas Canadians can’t cease excessive climate, we are able to work collectively to forestall it from worsening inequality. Rising consciousness, lowering losses, closing insurance coverage gaps and constructing resilience are key to defending these at biggest danger.

{Photograph}: A employee walks in a devastated neighborhood in west Jasper, Alberta, Monday, Aug. 19, 2024, after a wildfire brought about evacuations and widespread harm within the Nationwide Park and Jasper townsite. (Amber Bracken/The Canadian Press by way of AP)

This text is republished from The Dialog beneath a Artistic Commons license. The Dialog is an impartial and nonprofit supply of stories, evaluation and commentary from tutorial specialists. The unique article might be accessed right here.