")

{kind=link}

(Up to date on January 29, 2025 with screenshots from H&R Block Deluxe downloaded software program for the 2024 tax yr.)

A Mega Backdoor Roth is totally different from an everyday Backdoor Roth. It’s executed by making non-Roth after-tax contributions to a 401k-type plan earlier than transferring it to the Roth account throughout the 401k-type plan or taking the cash out (with earnings) to a Roth IRA.

It’s an effective way to place further cash right into a Roth account with out having to pay a lot further tax. Not all plans enable non-Roth after-tax contributions however some estimated that 40% of individuals can do it.

Suppose you probably did a Mega Backdoor Roth final yr. You must have acquired a 1099-R kind out of your 401k plan supplier. You’ll must account for it in your tax return. Right here’s find out how to do it in H&R Block tax software program. Should you use TurboTax or FreeTaxUSA, please see:

Use H&R Block Obtain

The screenshots on this publish are from H&R Block Deluxe downloaded software program. The downloaded software program is each cheaper and extra highly effective than the net model. A person reported getting an error from the net model of H&R Block in remark #8. The H&R Block downloaded software program didn’t give that error.

Should you haven’t paid to your H&R Block on-line submitting but, you should buy H&R Block downloaded software program from Amazon, Walmart, Newegg, or Workplace Depot and change to the downloaded software program. Should you’re already too far alongside together with your entries, make this your final yr of utilizing the net model and change to the downloaded model subsequent yr.

Inside the Plan Or To Roth IRA

You are able to do the mega backdoor Roth in two methods — convert throughout the plan or withdraw to a Roth IRA. Changing throughout the plan is way simpler, and lots of plans automate the method. Transferring to a Roth IRA additionally works. See the earlier publish Mega Backdoor Roth: Convert Inside Plan or Out to Roth IRA?

Right here’s the situation we’ll use for instance:

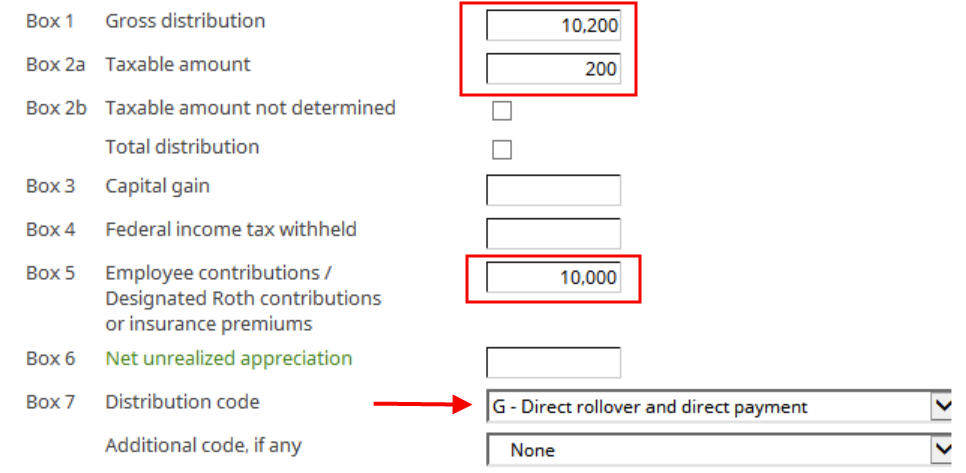

You contributed $10,000 as non-Roth after-tax contributions to your 401(ok). By the point you transformed the cash to the Roth account throughout the plan or transferred it to your Roth IRA, your contributions earned $200. You transformed $10,200 to your Roth account.

I’m utilizing 401(ok) as a shorthand. It really works the identical in a 403(b). Should you did a cut up rollover — after-tax contributions to a Roth IRA and the earnings to a Conventional IRA — and the plan administrator issued one 1099-R to your two rollovers, you’ll want to separate your 1099-R into two. See One 1099-R Type for Two Rollovers in TurboTax and H&R Block.

1099-R Entries

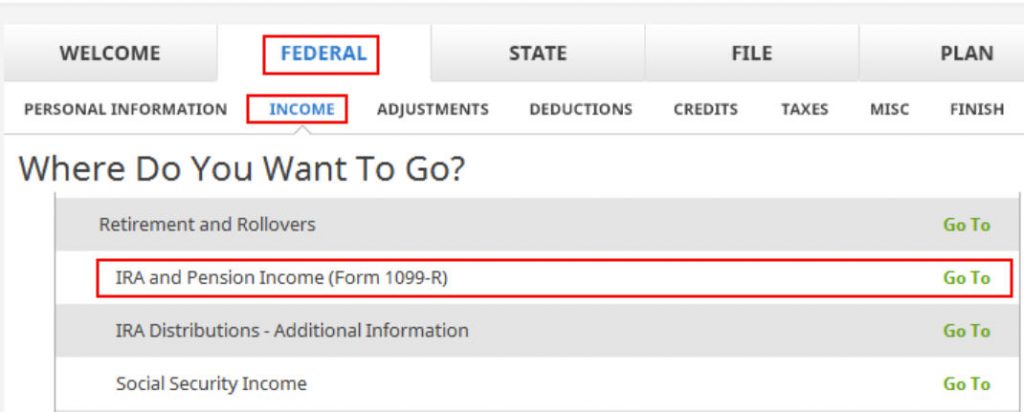

Go to Federal -> Earnings -> IRA and Pension Earnings (Type 1099-R). You may import the 1099-R or enter it manually. I’m exhibiting guide entries.

Our 1099-R is a standard 1099-R. Enter the numbers out of your 1099-R as-is. Ours seems like this:

The gross quantity transformed to the Roth account exhibits up in Field 1. The earnings are in Field 2a. Should you didn’t have earnings in your rollover, Field 2a is zero. “Taxable Quantity Not Decided” underneath Field 2b is left unchecked. The quantity of your non-Roth after-tax contributions exhibits in Field 5. Field 7 has code G.

The IRA/SEP/SIMPLE field in Field 7 in your 1099-R ought to NOT be checked.

We’re not a retired public security officer.

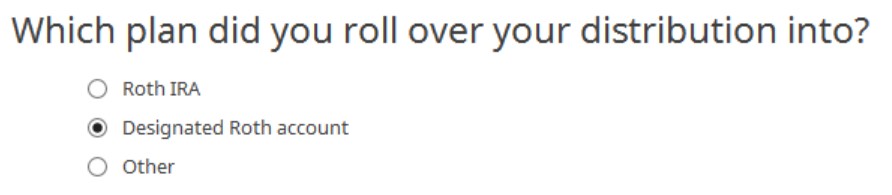

Rollover Vacation spot

The Roth 401k account is formally a “designated Roth account” within the plan. Select “Designated Roth account” for those who transformed throughout the plan. Select “Roth IRA” for those who took the cash out of the plan to your Roth IRA.

That’s it. It’s so simple as that.

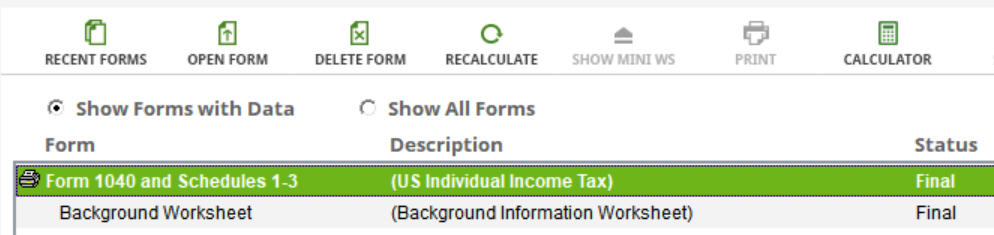

Confirm on Type 1040

Now we confirm we’re taxed solely on the $200 in earnings, and never on the $10,000 non-Roth after-tax contributions.

Click on on “Types” within the prime menu bar. Double-click on “Type 1040 and Schedules 1-3” within the kinds record and click on on “Conceal Mini WS.”

Scroll down to seek out Line 5. The gross quantity transferred to the Roth account exhibits on Line 5a. Line 5b exhibits you’re taxed solely on the earnings. Should you didn’t have earnings, Line 5b will likely be zero.

Once you’re executed trying on the kind, shut the kinds window to get again to the interview.

Say No To Administration Charges

If you’re paying an advisor a proportion of your property, you might be paying 5-10x an excessive amount of. Learn to discover an impartial advisor, pay for recommendation, and solely the recommendation.