{kind=link}

Social Safety offers everybody an official “Full Retirement Age.” It’s 67 for these born in 1960 or later, however you may declare as early as age 62, as late as age 70, or anyplace in between. The tradeoff is between a decrease month-to-month profit for extra years and a better month-to-month profit for fewer years. The uncertainty lies in how lengthy you’ll stay.

Every time there are decisions and uncertainty, folks attempt to optimize. Everyone seems to be searching for the holy grail — when to say Social Safety to maximise the advantages. However how a lot does it matter, anyway?

Open Social Safety

When you’ve paid consideration to this matter, you’d know Open Social Safety. It’s the very best instrument for a Social Safety claiming technique, and it’s utterly free.

The first enter in Open Social Safety is your Main Insurance coverage Quantity (PIA), which you acquire by creating an account with the Social Safety Administrationcopying your earnings historical past, and pasting it into ssa.instruments. See extra detailed steps in Retiring Early: Impact on Social Safety Advantages. When you’re married, each of it is best to undergo this course of to get your separate PIAs.

Open Social Safety makes use of your PIA, marital standing, gender, and date of start — and the identical in your partner in case you’re married — to calculate a really helpful technique. For instance, it produced this output for somebody single, male, born on 4/15/1960, with a $3,000 PIA:

You file in your retirement profit to start 10/2025, at age 65 and 6 months.

The current worth of this proposed resolution can be $416,562.

Open Social Safety tells you precisely when to say Social Safety, which is nice, however don’t cease there. In any other case, you’ll miss this calculator’s finest characteristic.

Spectrum Chart

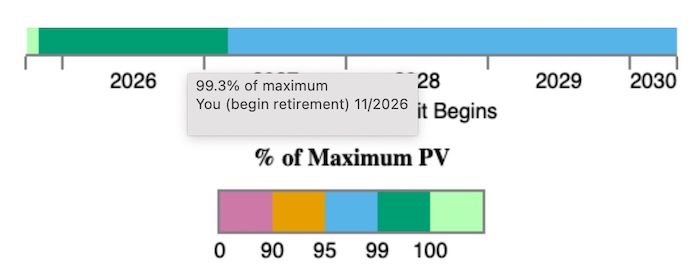

Scroll right down to the underside of the web page. You see a spectrum chart exhibiting how a lot the current worth of the advantages would change in case you begin your Social Safety on different dates. As you progress the mouse alongside the spectrum chart, the tooltip exhibits a proportion of the utmost for that begin date.

Open Social Safety recommends claiming instantly on this instance, however the spectrum chart exhibits that this individual would nonetheless get 99.3% of the utmost current worth in the event that they wait one other 12 months. And the worst case for this individual? Claiming at age 70 will get 95.2% of the utmost current worth.

The spectrum chart and the overall current worth reply this vital query:

How a lot does when to say Social Safety matter?

The whole current worth of Social Safety advantages claimed on the most optimum time is $416,562 for this individual within the instance. This tells them how a lot Social Safety performs a job of their retirement funds. If this individual has a $1 million internet value, Social Safety represents near 30% of the overall. Claiming on the worst time and getting 95% of the utmost current worth decreases the overall by 1.5%. I’m not suggesting that one ought to throw away 1.5% willy-nilly, however I’d say it’s effectively inside the margin of error.

Warmth Map

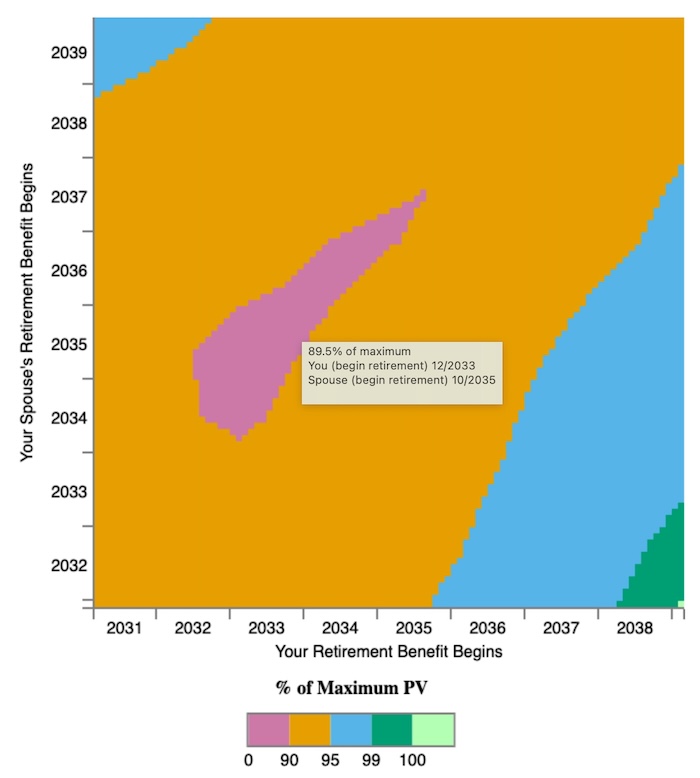

It’s extra difficult for a married couple. The one-dimensional spectrum chart for a single individual turns right into a 2D warmth map for a married couple. I ran one other case for example, which produced this chart:

The horizontal axis represents one partner, and the vertical axis represents the opposite partner. The really helpful technique is on the backside proper. One individual ought to delay till age 70, and the opposite individual ought to declare as quickly as attainable, which is a typical technique for a lot of married {couples}. The utmost internet current worth of their advantages is about $800,000.

The inexperienced and blue zones on the decrease proper of the warmth map point out that this couple has vital leeway in when to say. So long as one individual claims early, the opposite individual can declare at any time inside a 3-year vary (going horizontally on the backside), and they’d nonetheless get greater than 95% of the utmost current worth. Or so long as one individual delays till 70, the opposite individual can declare at any time inside a 5-year vary (going vertically on the proper edge), and they’d nonetheless get greater than 95% of the utmost current worth.

The magenta patch within the center represents the worst combos of claiming dates. In the event that they didn’t know any higher they usually picked the completely worst claiming dates, they might get 89.5% of the utmost current worth.

How a lot claiming dates matter for this couple relies on how a lot they’ve exterior Social Safety. If they’ve a $1 million internet value, Social Safety represents near 45% of their whole assets ($800k over $1.8 million whole). Selecting the worst claiming dates would put a 4.5% dent of their retirement, which is extra significant than the 1.5% within the earlier instance, but when they will hold it above 95% within the blue and inexperienced zones, I’d say that the impact of claiming dates falls effectively inside the margin of error.

Shifts in Technique

Open Social Safety makes use of a market rate of interest to calculate the current worth of the Social Safety advantages. Rate of interest adjustments can have an effect on the really helpful claiming technique. Typically persons are stunned to see a giant shift within the suggestion once they run the calculator once more at a later time. For instance, it used to advocate claiming at age 70, and now it recommends claiming at 68.

I wouldn’t fear about it if the earlier suggestion continues to be inside the blue and inexperienced zones. The purpose of utilizing Open Social Safety isn’t to get a single “finest” claiming technique. Mike Piper, the creator of Open Social Safety, stated this in his weblog put up in 2020:

What issues most isn’t selecting the perfect technique. What issues most is simply avoiding a very dangerous one. There are normally loads of methods which are virtually nearly as good as the perfect technique.

Open Social Safety makes use of mortality tables for the chance of your residing to every age. Pretty much as good as it’s, it nonetheless solely calculates based mostly on chances. No calculator is aware of if you’ll die. The perfect technique from any calculator received’t be the very best in case you defy the chances.

Make It Not Matter

Right here’s how I’d use Open Social Safety with my Make Fewer Issues Matter method:

1. Learn the utmost current worth output from Open Social Safety. Calculate its weight within the whole retirement assets.

Social Safety / (Social Safety + Non-Social Safety)

2. Be aware of the inexperienced and blue zones within the warmth map. All claiming dates within the inexperienced and blue zones give above 95% of the utmost current worth. Search for the worst case as effectively.

3. Mix (1) and (2) to comprehend the massive leeway in when to say Social Safety.

Claiming dates don’t matter so long as you keep within the inexperienced and blue zones within the chart. Write down the place your inexperienced and blue zones are. Save the chart picture in case you’d like.

Even the worst dates don’t matter if (a) the burden of Social Safety is small enough in your whole retirement assets; and (b) the worst dates nonetheless offer you near 90% of the utmost.

After all, you don’t select the worst dates on goal, however it’s a aid to know the way little it issues, and it’s not attainable to screw up too badly. You choose a spot within the inexperienced and blue zones, cross it off your thoughts, and transfer on to extra necessary issues.

Study the Nuts and Bolts

I put every part I exploit to handle my cash in a e-book. My Monetary Toolbox guides you to a transparent plan of action.