{kind=link}

When each spouses in a married couple retire earlier than 65, they most certainly will purchase medical health insurance from the ACA market until they’ve retiree medical health insurance protection or they solely have a brief hole that may be lined by COBRA. When there’s an age distinction between the 2 spouses, the older partner will begin Medicare at 65, leaving the youthful partner in ACA medical health insurance.

Reader Charlie introduced up this precise situation. Each Charlie and his spouse have ACA medical health insurance now. After Charlie turns into eligible for Medicare subsequent yr, his 58-year-old spouse will proceed on the ACA plan. Now, once they change from protecting each of them on the ACA plan to protecting only one particular person, how will their ACA medical health insurance premiums change?

Will their premiums drop 50%, as a result of they are going to cowl only one particular person as a substitute of two? Or really greater than 50%, as a result of the particular person coming off the plan, Charlie, is older and dearer to insure?

Will their premiums keep the identical, as a result of ACA premiums are tied to revenue, and their revenue received’t change?

Will their premiums really improve, or drop, however by lower than half, as a result of if it isn’t bizarre and counterintuitive, it wouldn’t make an fascinating topic for a weblog publish?

The reply is — the entire aboverelying on whether or not they obtain a subsidy and what plan they’ve.

We’re not speaking about premium will increase from the insurance coverage firm or modifications to the premium tax credit score from modifications in revenue. Simply altering the variety of individuals lined by an ACA well being plan can have bizarre and sudden results.

No Subsidy

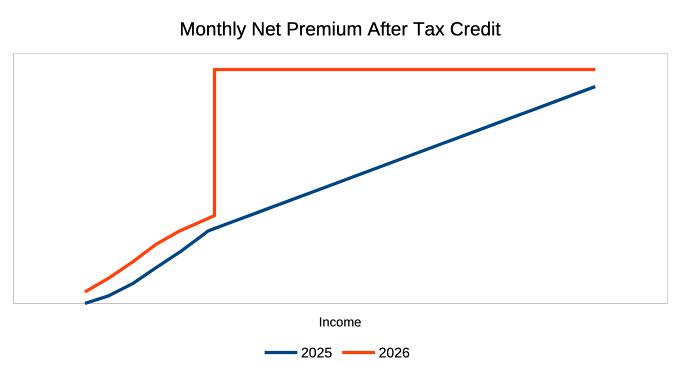

The ACA premium subsidy cliff is scheduled to return in 2026. The current authorities shutdown didn’t push it out. You received’t obtain any premium subsidy in case your revenue is above 400% of the Federal Poverty Degree (FPL), which is $84,600 in 2026 for a two-person family within the decrease 48 states.

It’s extra intuitive if you don’t qualify for a premium subsidy. While you pay the total worth, insuring two individuals positive prices greater than insuring only one particular person. When the older partner begins Medicare, your ACA medical health insurance premiums will drop by half. As a result of it often prices extra to insure an older particular person, it’ll fall by barely greater than half.

Subsidy – 2nd Lowest Price Silver Plan

In case your revenue qualifies you for a subsidy, the subsidy is calculated from the premiums for the Second Lowest Price Silver Plan (SLCSP) in your space. If it occurs to be the plan you select, you’ll be requested to pay a set proportion of your family revenue for that plan. The federal government can pay the rest with a premium subsidy. See ACA Well being Insurance coverage Premium Tax Credit score Percentages.

The quantity you’re anticipated to pay towards a second lowest price Silver plan goes by the family measurement and family revenue. It doesn’t matter how many individuals within the family are on the coverage. When one particular person goes on Medicare, your family measurement doesn’t change. Nor does your family revenue. Subsequently, you’re nonetheless anticipated to pay the identical quantity.

Suppose your family revenue is just under the utmost that qualifies for the premium tax credit score for a two-person family, and also you select the second lowest price Silver plan in your space. Your internet premiums after the subsidy will probably be the identical whether or not you cowl each of you or just one particular person. The one distinction is that the premium subsidy turns into smaller when the full premiums earlier than the subsidy drop by half.

After the older partner begins Medicare, additionally, you will must pay for Medicare Half B and Half D, and presumably a Medicare Complement coverage. Your whole spending on well being insurance coverage will improve. However, as a result of the deductible and co-pay on Medicare are decrease than these on an ACA plan, your whole healthcare spending could lower. And since you’ll nonetheless obtain a subsidy if you cowl only one particular person, albeit a smaller subsidy than if you cowl two individuals, a subsidy remains to be a subsidy. You’re higher off with a subsidy and never seeing a premium drop than should you should pay the total worth.

Subsidy – Extra Costly Plan

While you qualify for a premium subsidy and also you select a dearer plan than the second lowest price Silver plan in your space, you pay 100% of the value distinction along with your regular internet premium. The method in your internet premiums is:

Earnings * Relevant Share + (full worth in your chosen plan – full worth for the Second Lowest Price Silver Plan)

When one particular person goes off the ACA plan, the value distinction additionally drops by half. Your premiums after the subsidy will go down by the lower within the worth distinction.

Suppose you select a Gold plan, and it’s dearer than the second lowest price Silver plan by $500 monthly for 2 individuals. You pay 100% of this $500 worth distinction. The worth distinction could change into $240 monthly if you cowl only one particular person. Subsequently you save $260 monthly when the older partner begins Medicare.

Subsidy – Much less Costly Plan

The alternative occurs if you select a cheaper plan. You obtain 100% of the value distinction as your price financial savings to cut back your regular internet premiums. Your internet premiums after the subsidy are:

Earnings * Relevant Share – (full worth for the Second Lowest Price Silver Plan – full worth in your chosen plan)

When one particular person goes off the ACA plan, your price financial savings drop by half. Your premiums after the subsidy will go up by the lower within the worth distinction.

Suppose you select a Bronze plan, and it’s cheaper than the second lowest price Silver plan by $400 monthly for 2 individuals. You obtain 100% of this $400 worth distinction. The worth distinction could change into $180 monthly if you cowl only one particular person. Subsequently you lose $220 monthly in price financial savings when the older partner begins Medicare, and your internet premiums will rise by $220 monthly.

You pay extra to cowl one particular person in a cheaper plan than to cowl two individuals. Such is the punishment for selecting a cheaper plan.

Impact on HSA Contributions

All Bronze ACA plans are eligible for HSA contributions beginning in 2026. While you select a Bronze plan, you go from household protection to single protection for HSA after one partner begins Medicare, and also you’ll have a decrease HSA contribution restrict. As a result of HSA contributions decrease your Modified Adjusted Gross Earnings (MAGI) for ACA medical health insurance, your MAGI will improve if you contribute much less to the HSA. The next MAGI means a decrease subsidy, or presumably dropping the subsidy altogether when your MAGI goes over the 400% FPL cliff.

***

Right here’s a abstract of all of the situations:

| Change in Internet Premiums | |

|---|---|

| No Subsidy | Lower by 50% or extra |

| Subsidy – 2nd Lowest Silver Plan | No change |

| Subsidy – dearer plan | Lower by 50%+ of the value distinction between your plan and the SLCSP |

| Subsidy – cheaper plan | Improve by 50%+ of the value distinction between the SLCSP and your plan, plus the impact from HSA contributions and MAGI |

Charlie and his spouse qualify for a premium subsidy, they usually need a Bronze plan. Their internet ACA plan premiums will go up considerably when Charlie begins Medicare. It’s counterintuitive, however that’s the way it works.

Be taught the Nuts and Bolts

I put every thing I take advantage of to handle my cash in a e-book. My Monetary Toolbox guides you to a transparent plan of action.