{kind=link}

As governments speed up digital public infrastructure (DPI) investments, guaranteeing equitable entry to digital ID is important to keep away from deepening current inequalities. On-line digital ID refers to programs that permit people to securely confirm their identification remotely for providers corresponding to banking, authorities packages, and digital transactions. But billions of individuals worldwide nonetheless lack entry to those programs: girls and marginalized communities particularly face vital gaps in each on-line digital ID possession and utilization. This weblog outlines key obstacles and 5 coverage actions to extend adoption, belief, and financial participation.

The financial case for on-line digital ID

The potential advantages of on-line digital ID are substantial for people, governments, and the non-public sector alike. McKinsey International Institute, based mostly on a pattern of seven nations, projected that governments can unlock as much as 13% of GDP by increasing digital ID programs. But, gender gaps in digital ID entry and utilization persist.

UN Ladies notes estimates that closing the gender digital divide would enhance the lives of 343.5 million girls and ladies, generate roughly US $1.5 trillion {dollars} by 2030, and elevate 30 million out of poverty by 2050. Globally, digital ID programs have the potential to extend digital funds by 22 p.c per 12 monthsenabling monetary service suppliers to assemble richer buyer knowledge and enhance service supply.

Nation-level proof reinforces these positive factors. Ethiopia’s ID Advantagesbuilt-in throughout checking account opening, SIM card registration, and authorized notary providers, diminished transaction occasions by 46–56 p.c. It additionally lower buyer acquisition prices by 4–48 p.c and lowered transaction prices for monetary service suppliers by 23–49 p.c. In Estonia, the federal government estimates its digital ID system saves greater than 1,400 years of working time yearly by means of streamlined public service supply. Past effectivity, digital IDs enhance comfort for customers, broaden entry to each private and non-private providers, and might strengthen privateness protections when designed responsibly.

What’s the digital ID hole?

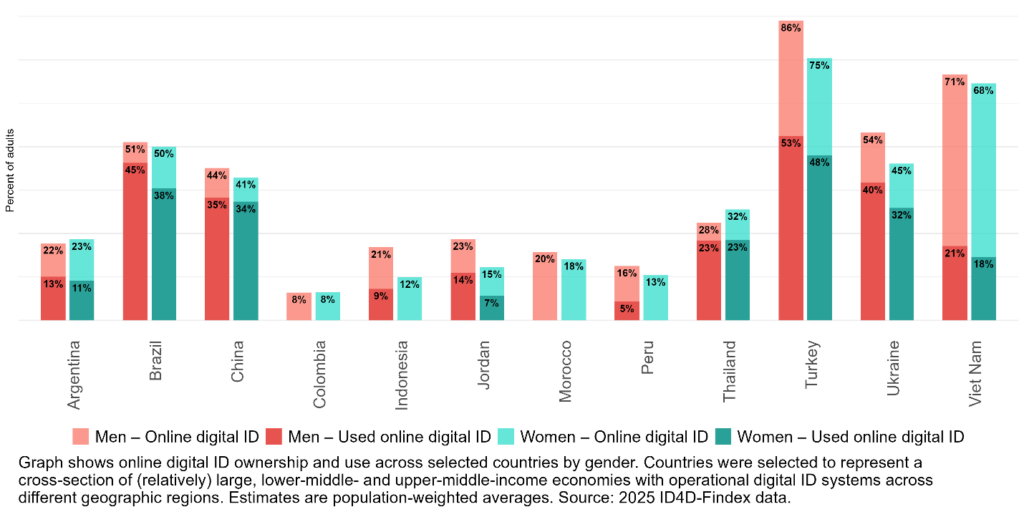

Ladies in lots of nations are disproportionately underrepresented in each digital ID possession and use. These figures level to a development that undermines efforts to construct extra inclusive digital monetary programs. Nation-level knowledge from the World Financial institution’s ID4D dataset reveal notable disparities (Determine 1). Important possession gaps are present in nations like Turkey (11 pp.), Ukraine (9 pp.), and Jordan (8 pp.), whereas vital utilization gaps are equally pronounced in nations together with Ukraine (8 pp.), Brazil (7 pp.), and Jordan (7 pp.).

These gaps mirror broader structural inequalities. Low digital monetary functionalitywhich disproportionately impacts girls, rural populations, and the aged, makes on-line enrollment, biometric seize, and digital authentication tougher. When compounded with restricted cellular web entry which an estimated 3.4 billion folks nonetheless lack, the result’s a cycle of exclusion that digital ID programs alone can’t break.

Some excellent news: progress on digital ID entry

The worldwide inhabitants with out entry to on-line digital ID decreased from 3.3 billion in 2021 to 2.8 billion in 2025.

In the present day, over half of the inhabitants with out entry to on-line digital ID (1.49 million) dwell in Decrease-Center Revenue International locations (LMICs), hindering their means to take part in digital economics and entry important providers.

Nevertheless, entry and possession are usually not all that issues. Even in nations that implement digital ID programs, particular person possession and utilization usually stay low. Amongst adults in growing nations with superior digital ID programs, 40 p.c report proudly owning a digital ID, whereas solely 30 p.c report having used it. These figures level to a important hole between the supply of digital identification infrastructure and its significant adoption.

Key obstacles to adoption and possession

Whereas the ID4D database doesn’t define obstacles to on-line digital ID possession and use, the International Findex Database factors to a number of interconnected challenges that may result in low digital ID uptake:

- Infrastructure constraints: Poor web connectivity, restricted cellular protection, and unreliable electrical energy hinder distant enrollment and authentication.

- Digital functionality gaps: Low ranges of digital and monetary literacy scale back the power of many customers to navigate enrollment and verification processes.

- Governance and belief deficits: Technical limitations, fragmented regulatory frameworks, and a scarcity of public belief in digital programs create additional resistance to adoption.

- Coordination challenges: Worldwide coordination on interoperable digital identification requirements stays restricted, slowing cross-border recognition and use.

Privateness issues, knowledge misuse, and unreliable infrastructure have an effect on each women and men, however girls face compounded challenges as a result of systemic inequalities. For instance, girls in low- and middle-income nations are 8 p.c much less probably than males to personal a cell phone, 14 p.c much less more likely to personal a smartphoneand 14 p.c much less probably to make use of cellular weblimiting their means to enroll and authenticate on-line. Coupled with governance and belief deficits, low digital functionality, and coordination challenges, on-line digital IDs can stay out of attain for a lot of.

Coverage actions for governments and regulators

To enhance each possession and significant utilization of on-line digital IDs, policymakers and regulators have to be intentional about design and supply. Bridging the hole between proudly owning a digital ID and actively utilizing it requires selections centered on probably the most weak populations. Key priorities embrace:

- Spend money on inclusive infrastructure: Increase digital connectivity, cellular protection, and electrical energy entry in underserved and rural areas to allow onboarding and authentication.

- Improve digital monetary functionality: Assist focused digital monetary functionality packages, particularly for girls and marginalized populations, to construct confidence in utilizing on-line digital ID programs.

- Undertake women-centered design rules: Combine options and outreach methods that mirror girls’s particular obstacles, wants, and preferences, corresponding to privateness safeguards, community-based registration, and simplified interfaces. See Ladies’s World Banking’s Coverage Handbook for Ladies’s Monetary Inclusion for extra info.

- Use simplified digital know-your-customer (e-KYC) processes: Scale back documentation necessities and help different verification strategies to decrease obstacles for first-time customers. https://www.womensworldbanking.org/insights/policy-handbook-for-womens-financial-inclusion/

- Align with world requirements: Set up nationwide programs with worldwide frameworks that meet Monetary Motion Process Drive (FATF) requirements to safeguard shoppers’ privateness, security, and management over their private knowledge and guarantee usability throughout borders and platforms.

By guaranteeing that women and men world wide can each personal and meaningfully use their identification documentation, governments, improvement establishments, and the non-public sector can advance extra inclusive economies and societies.

By: Saniya Ansar (Economist with the Finance and Non-public Sector Analysis Staff of the Growth Analysis Group on the World Banok)Francesca Brown (Director of Coverage & Advocacy at Ladies’s World Banking), Victoria Johnson (International Coverage Advocacy Specialist at Ladies’s World Banking)and Jorin Margaux Wolff (Analysis Analyst with the World Financial institution’s Identification for Growth (ID4D) Initiative)