{kind=link}

As one other wildfire season looms, insurance coverage corporations have deserted some California neighborhoods at decrease threat of burning, forcing tens of hundreds of house owners to acquire bare-bones protection from the state’s insurer of final resort.

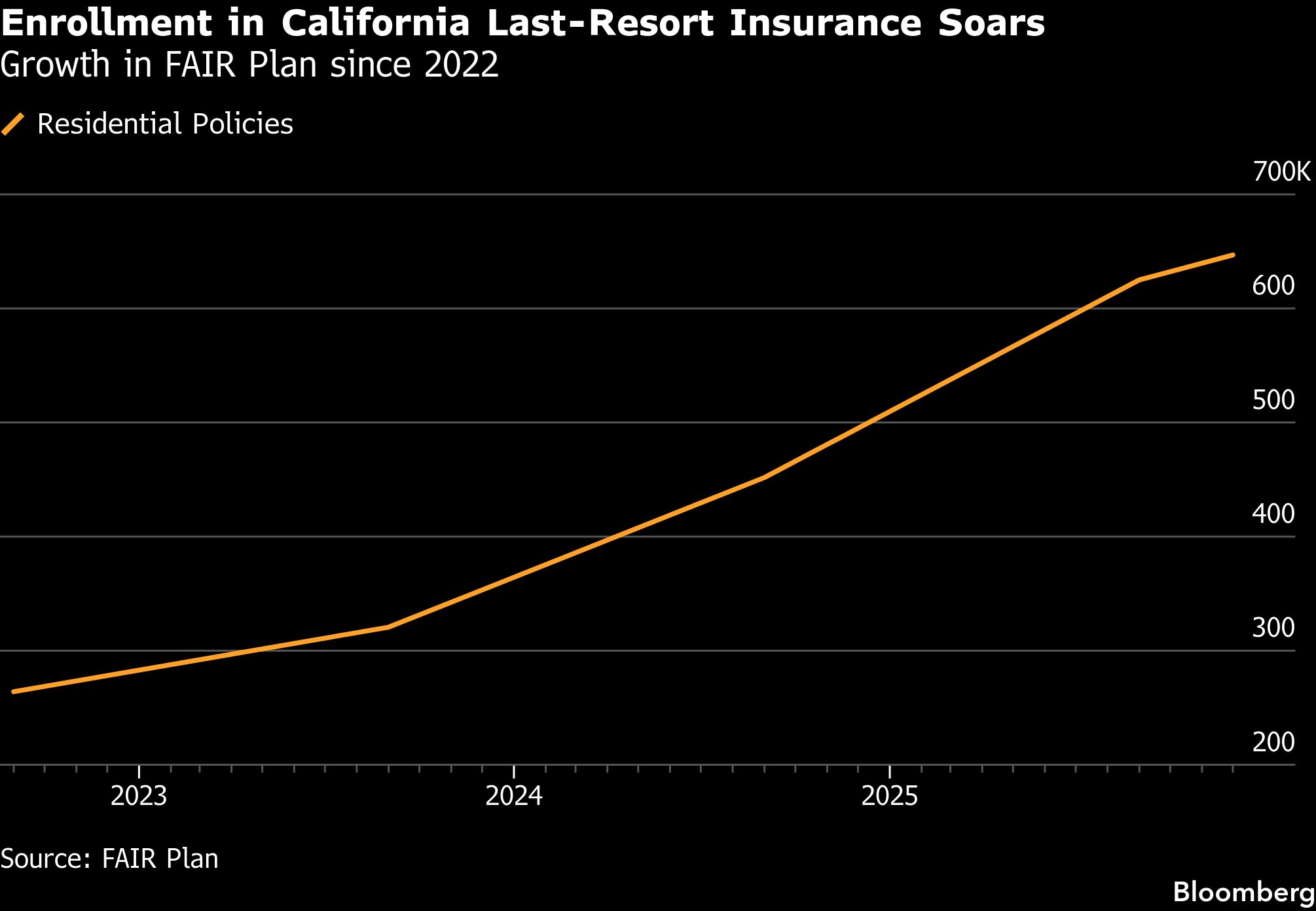

California supposed the insurer, referred to as the FAIR Plan, as a backstop for householders unable to safe insurance coverage on the personal market as a result of they dwell in areas of the state classifies as at excessive threat for wildfire on account of vegetation, terrain and climate. Between September 2024 and December 2025, enrollment in FAIR surged 43% as insurers pull again from California following a sequence of catastrophic wildfires, together with final 12 months’s $40 billion Los Angeles inferno.

Associated: ‘Nation’s First’ Smoke Injury Requirements Invoice Wending Via California Legislature

However in an indication insurers have curtailed protection even in locations much less prone to face wildfires, 14% of present FAIR insurance policies are for properties largely in city zones with low hearth threat, in keeping with a Bloomberg Information evaluation of FAIR plan information, with 28% of the cash-strapped plan’s publicity now in these areas.

“What we’re seeing is that the an infection of the market that existed within the high-fire-risk areas has unfold into the traditional elements of the market,” mentioned Michael Wara, director of the local weather and power coverage program at Stanford College.

A spokesperson for the FAIR Plan declined to remark.

California’s climate-driven insurance coverage disaster has spawned efforts to reform the state’s extremely regulated market, the place it might take insurers a 12 months or extra to acquire required approval for a price hike. Regulators have pledged sooner turnarounds and the granting of charges that mirror rising wildfire dangers to incentivize insurers to develop protection in high-hazard areas. However within the wake of the LA fires that destroyed 12,000 houses and left burned-out householders preventing insurers to get claims paid, state legislators at the moment are searching for to impose new mandates on the trade to right inequities revealed by the catastrophe.

Associated: 9 Claims Traits to Watch Via The Remainder of 2026

Specialists say California might show a testing floor for a carrot-and-stick method to stopping the collapse of insurance coverage markets as rising wildfires, hurricanes and different local weather disasters shake up the trade in different states.

“The insurance coverage market proper now’s in a fragile state,” mentioned Mark Sektnan, vp for state authorities relations at trade advocacy group American Property Casualty Insurance coverage Affiliation. “The selections that the legislature makes via the legal guidelines that they go might make California both look like a extra encouraging market or much less encouraging marketplace for insurers wanting to come back again.”

One lately launched invoice would require insurers to offer and renew insurance policies in high-risk areas for householders that make their dwellings extra fire-resilient or threat being suspended from doing enterprise in California for 5 years. Many LA householders found they had been severely underinsured and different laws would order insurers to supply assured substitute of a destroyed home.

A spokesperson for State Farm, California’s largest insurer by market share, declined to remark.

Associated: State Farm’s 17% California Owners Fee Hike to Stay Underneath New Settlement

One other invoice, backed by California Insurance coverage Commissioner Ricardo Lara, would enable the FAIR plan to supply complete protection. The plan, which now writes practically 10% of residential insurance policies within the state, at the moment can solely present hearth insurance coverage and householders should purchase insurance policies elsewhere to cowl different injury. Specialists say shifting householders off FAIR and again to non-public insurers is essential to restoring a wholesome market however the laws might make the plan a extra enticing various than conventional insurance coverage.

“The FAIR Plan was by no means designed to be pretty much as good because the safety you could get within the personal market as a result of we don’t need folks on FAIR,” mentioned Amy Bach, government director of United Policyholders, a San Francisco nonprofit that advocates for householders.

Michael Soller, a deputy California insurance coverage commissioner, mentioned the intention of the laws is to offer householders the protection they want when “they must be on the FAIR Plan, however that must be brief time period.”

A FAIR spokesperson mentioned the plan is reviewing the invoice however had no remark.

Sektnan mentioned the expansion of last-resort insurance coverage in California, together with in lower-fire-risk areas, is due partly to its comparatively low premiums. “You’ll be able to’t depopulate the FAIR Plan if it’s competitively priced or if it’s priced decrease than what’s available in the market,” he mentioned.

There are tentative indicators, although, that entry to the personal market is bettering. After breakneck progress within the FAIR Plan since 2024, enrollment elevated by lower than 4% within the last three months of final 12 months. The California Division of Insurance coverage has lately accepted or is at the moment contemplating price improve requests from six main insurers below its “sustainable insurance coverage technique” that guarantees faster critiques of proposals in trade for commitments to develop protection in high-risk areas.

“Insurance coverage corporations are coming into the division detailing their plans to really keep and what we’re seeing are preliminary alerts of market turnaround and progress,” mentioned Soller.

As an example, the state’s second-largest insurer by market share, Farmers Insurance coverage Group, has requested for an almost 7% price hike. To safe that improve, it has pledged to market to 300,000 shoppers residing in high-risk wildfire zones starting in 2026 and so as to add about 5,600 insurance policies in these areas over two years, in keeping with an insurance coverage submitting. The fifth-largest insurer, CSAA Insurance coverage Group, famous in its 2025 price request that it has issued 18,300 extra insurance policies in high-fire-hazard areas than the state requires.

No. 3 insurer Mercury Common Corp. set a goal so as to add 15% extra insurance policies in high-risk areas over the following two years in its submitting for a price improve final 12 months. The corporate mentioned that its eight-year aim is to shift 6.5% of FAIR Plan policyholders to its personal insurance policies.

Insurance coverage trade consultant Sektnan mentioned the market received’t get better with out even sooner critiques of price hike petitions as in any other case inflation erodes the worth of premium will increase.

Testifying earlier than a state legislative committee in February, Lara instructed lawmakers the insurance coverage division has accomplished current price hike assessments in 120 days and now’s focusing on a 60-day evaluate. “We’re not out of the woods,” he mentioned. “A structurally more healthy market is a 3–5-year challenge.”

High picture: Firefighters battle flames in the course of the Palisades Fireplace in Los Angeles on Jan. 7, 2025. Photographer: Kyle Grillot/Bloomberg.

Copyright 2026 Bloomberg.

Subjects

Traits

California